Contents Provided by Media OutReach

“Coface China Corporate Payment Survey 2022 : Longer payment delays and rising credit risks in some sectors”

HONG KONG S.A.R. - Media OutReach - 11 MAY 2022 – Coface's 2022 China Corporate Payment Survey[1] shows that fewer firms encountered payment delays in 2021, but those that did report longer periods of overdue payments than in the previous year. The average payment delay rose from 79 days in 2020 to 86 days in 2021. Firms in 9 out of 13 sectors reported an increase in payment delays, led by agri-food, which recorded the largest increase of 43 days, followed by wood, transport, and textile.

More companies are reporting ultra-long payment delays (ULPDs), which are payments overdue by more than six months, rising from 15% to 19% in 2021. More worrying, there was a significant increase in those facing ULPDs exceeding 10% of their annual turnover, jumping from 27% in 2020 to 40% in 2021, notably the construction and agri-food sectors.

With China's economic growth projected to slow in 2022, fewer companies are expecting an improvement in sales and cash flow.

Coface expects China's GDP growth to slow to 4.8% in 2022, following a strong 8.1% in 2021, as the Chinese economy continues to face significant headwinds to growth, including a property sector downturn, the pursuit of zero-COVID policies, subdued consumption recovery, and higher commodity prices.

Bernard Aw, Economist for Asia Pacific at Coface, said:

"Coface's latest China Corporate Payment Survey showed credit terms offered by Chinese companies remained tight despite a recovery in the Chinese economy in 2021, as companies remain cautious due to the ongoing pandemic. Agri-food and energy made the biggest cut (-23 days each), reflecting increasing credit risks linked to rising raw material prices.

"Although fewer companies reported payment delays, there was a rise in the proportion of respondents reporting that payment delays had increased, from 36% in 2020 to 42% in 2021, the highest since 2016. Agri-food reported the largest surge in average payment delays (43 days) to reach 88 days. Upward trends were reported in wood (+20 days), transport (+18) and textile (+16), highlighting the impact of slower domestic demand due to strict social distancing restrictions in China.

Chinese firms are less optimistic about China's economic prospects, with 44% of respondents expecting sales to improve this year, down from 65% in 2020, while those forecasting better cash flow fell by nearly half from 50% in 2020 to 27% in 2021. Rising raw material prices, a weakening market demand, and the ongoing pandemic were key factors as reported by respondents.

"The recent outbreak of Omicron demands more Covid control in China and it will worsen the global supply chain disruptions. Coface expects corporate bond defaults and insolvencies in China to increase in 2022, especially among sectors that accumulated higher cash flow risks in 2021 due to the pandemic."

Payment delays[2] : Rising raw material prices become a key factor in overdue payment

Fewer companies experienced payment delays in 2021, with 53% of respondents reporting overdue payments, down from 57% in 2020. However, the average payment delay rose from 79 days in 2020 to 86 days in 2021. Construction continued experiencing the longest payment delays with 109 days, followed by 99 days for transport.

Most worrying, the share of respondents experiencing ultra-long payment delays (ULPDs) exceeding 2% of annual turnover expanded from 47% in 2020 to 64% in 2021. Construction remained the sector with the highest share (56%) of respondents reporting ULPDs exceeding 10% of their annual turnover. According to Coface's experience, 80% of ULPDs are never paid. When they constitute a share of annual turnover above 2%, a company's cash flow could be at risk.

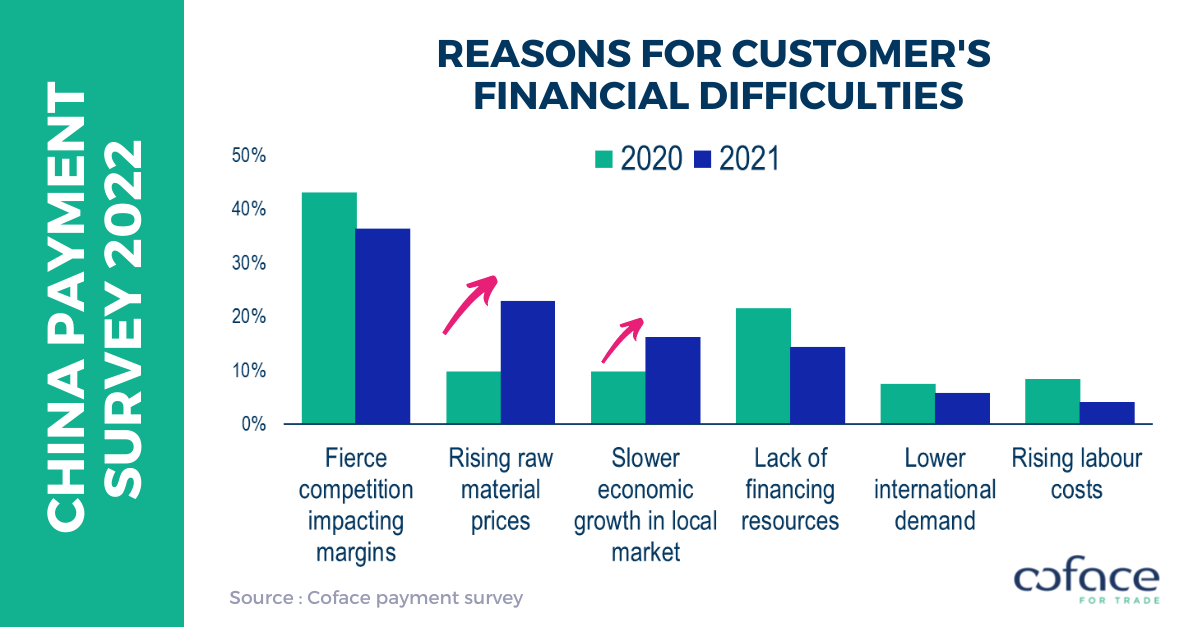

The main reason behind those delays remains customers' financial difficulties, highlighted by nearly three-quarters of respondents that indicated payment delays. Financial difficulties were caused mostly by fierce competition affecting margins (36%), but also - to a greater extent in 2021 - by rising raw materials prices (23% vs. 10% in 2020) and a slowdown in local market growth (16% vs. 10% in 2020). This reflects rising commodity prices are placing pressure on operational costs which directly impacts companies' cash flow.

Economic expectations: Hopeful, but significant growth risks remain

Looking ahead, the majority of respondents remained hopeful about economic prospects in the year ahead, although the share of optimists was down to 68%, from 73% the previous year

Expectations about sales and cash flows were less sanguine, which may be connected to a tapering of recovery momentum as businesses move closer to pre-pandemic conditions. The percentage of respondents anticipating improved sales performances in the coming year shrank from 65% in 2020 to 44% in 2021, while those forecasting better cash flow fell by nearly half from 50% in 2020 to 27% in 2021. Rising raw material prices, a weakening market demand, and the ongoing pandemic were key factors highlighted by respondents that expected weaker sales performances.

Coface expects China's GDP growth to slow to 4.8% in 2022, following a strong 8.1% in 2021, as the Chinese economy continues to face significant headwinds to growth, including a property sector downturn, the pursuit of zero-COVID policies, subdued consumption recovery, and higher commodity prices.

Global supply chains likely to remain tight

The effects of the Russia-Ukraine crisis and China's zero-COVID measures are expected to deliver another hit to global supply chains. With the prominent role played by both Russia and Ukraine in the global energy and food markets, the crisis is a significant risk to the supply of such commodities. Russia is the second- and third-largest world producer of gas and oil, respectively. It is also a major producer of strategic metals, such as palladium, nickel and copper. These metals are used in the automotive and aircraft industries, while copper is an important metal for the construction sector. Both countries are important exporters of certain agricultural commodities, notably for sunflower and safflower oil (75% of global exports in 2019 combined), wheat (29%), coarse grain (20%) and corn (19%). Sanctions on Russian commodities, including an import ban on Russian crude and refined products by the United States, the United Kingdom, Canada and Australia, as well as the European Union (EU)'s import restrictions on Russian iron and steel, raised fears of the reduced availability for such products, resulting in rising prices. Financial sanctions on several Russian banks and restrictions on access to U.S. dollars could affect agricultural trade flows. Disruptions to trade routes also added to concerns about higher prices and delivery delays.

While China has shifted from a strict zero-COVID strategy to a 'dynamic' approach in order to minimize adverse impacts on the Chinese economy, negative effects, arising from measures implemented to contain outbreaks across the country, remain. The lockdowns in Shenzhen and Shanghai in March and April have impacted the normal operations of landside logistical and warehouse services, despite port operations continuing to function. This has already intensified pressure on supply chains during March. China PMI suppliers' delivery times index fell to a two-year low in March 2022, reflecting worsening delivery delays. Similarly, China's Logistics Industry Prosperity Index also declined to the lowest since February 2020, with the logistics sector affected by the spread of the pandemic in multiple parts of the country, where differentiated pandemic management measures disrupted cross-regional distribution and the ability to maintain a smooth flow.

- The 2022 China Corporate Payment Survey was conducted between November 2021 and January 2022, and surveyed over 1,000 companies across 13 broad sectors located in mainland China.

- Payment delay – the period between the due date of payment and the date the payment is actually made.

Download the full report here

COFACE: FOR TRADE

With over 75 years of experience and the most extensive international network, Coface is a leader in trade credit insurance and adjacent specialty services, including Factoring, Single Risk insurance, Bonding, and Information Services. Coface’s experts work to the beat of the global economy, helping ~50,000 clients in 100 countries build successful, growing, and dynamic businesses. With Coface’s insight and advice, these companies can make informed decisions. The Group' solutions strengthen their ability to sell by providing them with reliable information on their commercial partners and protecting them against non-payment risks, both domestically and for export. In 2021, Coface employed ~4,538 people and registered a turnover of €1.57 billion.

#Coface

The issuer is solely responsible for the content of this announcement.

Latest comments