Spooked by a massive exodus of Chinese capital in 2015, the country’s policymakers hit on a plan to alleviate pressures on their currency. They could attract foreign cash—and boost demand for the yuan—by opening the doors to fixed income investors. Big overseas funds are always looking for ways to diversify and would likely want some exposure to China’s bond market, the third-largest in the world.

Money poured in, and inflows accelerated after China set up a channel called Bond Connect for foreigners to trade through Hong Kong in July 2017. But overseas funds started pulling money out in late 2018.

They’ve cooled on a market that in some ways is proving its worth as a diversification play. China’s government bonds were among the world’s best performers in 2018, returning 7.7 percent, while U.S. Treasuries earned 0.8 percent, ICE Bank of America Merrill Lynch data show. That gain is in yuan terms, however, and the yuan dropped 5.4 percent against the U.S. dollar.

Greater access to China’s markets hasn’t been enough to overcome geopolitical worries. The U.S.-China trade war has hurt the yuan and may also be giving foreigners pause before they add to their Chinese bond holdings, market watchers say. U.S.-based investors trimmed their participation in the country’s dollar-denominated sovereign bond sale in October. They accounted for only 2 percent of the five-year notes China issued, down from 20 percent in 2017. And China’s biggest bank, Industrial & Commercial Bank of China Ltd., canceled a dollar bond sale in the U.S. in November.

China’s policymakers will keep trying to attract bond investors, and Goldman Sachs Group Inc. anticipates a fresh campaign by China to promote its currency. Part of this involves overhauling regulations to win inclusion for Chinese bonds in global bond indexes. A key milestone may come in April: That’s when China debt will start to be included in the Bloomberg Barclays Global Aggregate Index, assuming certain criteria for accessibility and transparency are met. There’s room for demand to grow: The main non-Chinese buyers of the bonds so far have been sovereign wealth funds and central banks, with “very few” nonofficial asset managers getting in, according to Morgan Stanley.

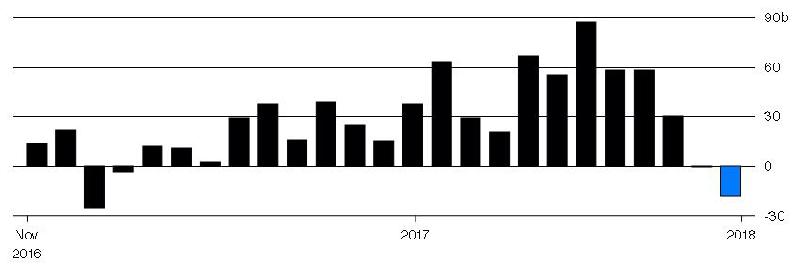

Foreign Investors’ Holdings of Chinese Bonds

Monthly change, in yuan

Data: ChinaBond, Bloomberg

“Capital inflows, especially those into the bond market, will be very crucial for China’s balance of payments, as the current account will deteriorate further amid the trade war and the restructuring of the economy,” says Becky Liu, head of China macro strategy at Standard Chartered Plc in Hong Kong. China’s trade surpluses are subsiding, and some economists even expect the country in coming years to shift to sustained current account deficits. If China’s bond market receives waves of overseas cash, that will help finance the deficits without running up a dangerous amount of debt in foreign currency.

Estimates on inflows in coming years vary widely, from about $760 billion over the long term at Morgan Stanley to Goldman’s $1 trillion by the end of 2022 to $3 trillion through 2020 at UBS Asset Management. Jason Pang, a fixed income portfolio manager at JPMorgan Asset Management in Hong Kong, says his company has been boosting China holdings in recent months. “Whether we will add more,” he says, “depends on the trade war.”

Source: Bloomberg

Latest comments