An economic slowdown and extremely tight credit conditions pushed corporate debt to a record high in China last year, according to experts.

Defaults for Chinese corporate bonds — issued in both U.S. dollars and the Chinese yuan — soared last year, according to numbers from two banks.

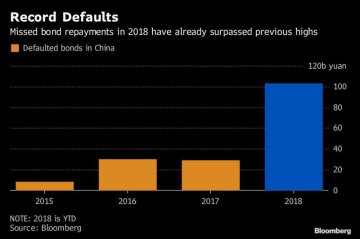

Yuan-denominated debt rose to an "unprecedented" 119.6 billion yuan ($17.8 billion) — four times more than 2017, according to a February report by Singapore bank DBS.

Japanese bank Nomura's estimates, provided to CNBC, were even higher, putting the size of defaults in onshore bonds — or yuan-denominated bonds — at 159.6 billion yuan ($23.8 billion) last year. That number is roughly four times more than its 2017 estimate.

Offshore corporate dollar bonds, or U.S. dollar-denominated debt issued by Chinese companies, followed the same trend. Nomura said the amount of such debt rose to $7 billion in 2018, from none the year before.

"China witnessed an unprecedented wave of corporate bond defaults last year, in a fresh sign of wobbles hitting financial markets as slowdown deepens," said DBS analysts in the report.

According to DBS, the energy sector bailed on 46.4 billion yuan of payments in 2018 — making up almost 40 percent of all defaults in yuan-denominated debt. Consumer companies were the next worst hit, according to the bank's report.

"The default wave is extending into 2019 ... Given the reduced risk appetite and huge maturing volume, the outlook is poor," DBS said, adding that there are 3.5 trillion yuan in corporate bonds due this year.

High borrowing costs

Companies are facing tighter monetary conditions, aggravated by high borrowing costs, DBS said, adding that real interest rates shot up to 4.35 percent in January, from as low as 3.1 percent at the start of 2017.

"Availability of credit for refinancing remains tight despite repeated monetary easing by (the) PBOC," said DBS, referring to the People's Bank of China, the country's central bank. Meanwhile, it added: "Commercial banks have remained cautious in lending to private companies and financially wobbly state-owned enterprises."

Such tough monetary conditions "add to the financial stress on Chinese firms," DBS warned, saying it "doesn't bode well for their debt repayment ability."

The bank singled out the property sector and said that "a worryingly large share of recent borrowing has come in the form of short-term bonds." The funding pressure faced by property developers have been exacerbated by the housing slowdown, it added.

Last year's defaults hit mostly companies in the private sector as compared to the last cycle in 2016, according to Edmund Goh, Asian fixed income investment manager at Aberdeen Standard Investments.

"Rising rates environment in 2017 and early 2018 ... and in general, weaker economic growth in (the second half of 2018) were, of course, the main culprit for defaults — but why is it concentrated on private companies then? Because we see strong support policies in place to channel capital to Chinese state-owned-enterprises in the last few years," Goh explained.

As the U.S. economy has been robust, the Federal Reserve has been raising interest rates to prevent overheating in the world's largest economy. But as rates rise, bond prices fall and yields on U.S. dollar-denominated debt increase.

When the yuan fell steadily against the greenback last year, Chinese companies earning in the local currency found repaying debt in U.S. dollars much harder.

Crackdown on shadow lending

Analysts also blamed the record high default rate on the crackdown on shadow banking, which left private companies with less cash flow and hence unable to pay their debts.

Shadow banking refers to activities performed by financial firms outside the formal banking sector, and therefore subject to lower levels of regulatory oversight and higher risks.

"We have to remember that in the past, regulations were more relaxed on shadow banking lending. Private companies relied on those when they couldn't issue bonds. But (the) government started cracking down on those in 2017," said Aberdeen's Goh.

The situation has worsened since the shadow banking system is the "primary credit provider for the low-quality corporates in China," said Tiansi Wang, senior credit analyst at asset management firm Robeco.

State-owned banks usually prefer lending to companies owned by the government, which are considered safer borrowers than private firms. As a result, many private companies have turned to shadow banking.

Defaults look set to continue this year although at a more manageable pace, said experts.

But that doesn't bode well for already-high debt levels in China, which analysts have said is set to increase this year, as Beijing looks to increase lending amid easing measures to boost its economy.

However, that's at least one bright spot for companies in desperate need of funds.

Goh, pointing to efforts by Chinese authorities to encourage banks to lend more, said that will "help at least partially alleviate the extremely tight funding market for private companies in 2019."

"We think the easing rates environment will help the bond market in 2019 ... We also believe some of the tax cuts and fiscal policies will stimulate the economy this year," he said.

Source: CNBC

Latest comments