There’s plenty of bad debt to go around for investors in distressed assets in China. The question is how to extract value from them.

There’s plenty of bad debt to go around for investors in distressed assets in China. The question is how to extract value from them.For years, Chinese banks shoveled nonperforming loans to asset managers set up by the government, which sought to get back what they could while warehousing what was irrecoverable. Now, as commercial lenders try to shift record amounts of soured loans off their books, these assets are finding a home outside the state-sanctioned bad debt managers.

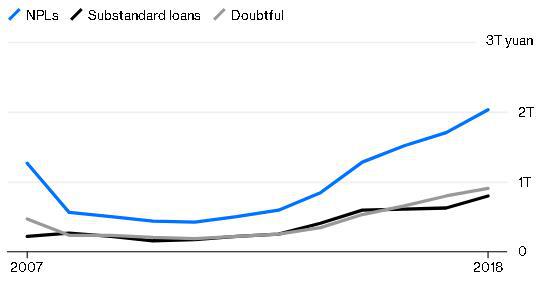

China’s big banks have cleaned up nonperforming loans with a face value of more than 900 billion yuan ($134 billion) by packaging them into securities, tapping foreign investment funds, selling them privately, or swapping them for equity. Beijing is welcoming overseas investors into the market and has set up trading exchanges for the assets. The financial system is sitting on lots more bad debt, though (as of December, China’s commercial banks held more than 2 trillion yuan, or close to $300 billion, of nonperforming loans) — and few of these methods are real, commercial solutions.

Up, Up and Away

Souring debt continues to rise across China's commercial banking system

Source: CEIC

Part of the problem, as we noted previously, is that prices of nonperforming assets are dropping as quality deteriorates and supply increases. Auctions of pools of soured debt are starting to fail, with some receiving zero bids. Last year, about 20 percent of such auctions didn’t result in a single sale. Either there were no bidders or the traditional buyers (read: bad-debt managers) weren’t willing to meet the benchmark price set by banks for their portfolios.

With that channel clogged, securitization is taking off. In theory, the bundling of loans into marketable securities deepens capital markets, helps banks clean up their books and allows companies to tap funding by monetizing their assets — all things China desperately needs. Issuance hit $290 billion last year, according to S&P Global Intelligence, led by banks and other finance companies. Paper backed by corporate receivables rose 117 percent while residential mortgage-backed securities grew even more.

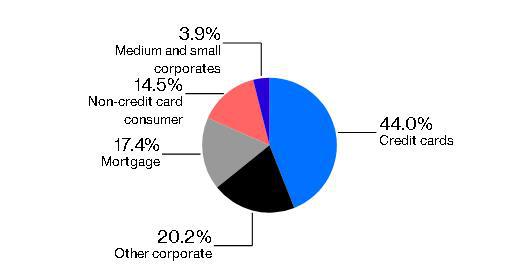

Souring Mood

Most securitized nonperforming loans are to consumers

Source: UBS

Declining prices may also threaten this avenue, though. As in Europe, banks in China are offloading pools of nonperforming mortgage, credit-card and other consumer loans. In Europe, NPLs change hands at about 30 percent of their gross book value. China’s securitized bad loans are selling at deeper discounts because the underlying asset prices are dropping. Target recoveries for subprime are between 0 and 10 cents on the dollar, based on a UBS Group AG analysis of 68 NPL securitization deals.

Even prime tranches only get recovery rates from about 10 cents or less (for credit cards) to 50 cents (for mortgages) on the dollar — not enough to inspire bad-debt managers to invest. The process of recouping value is also cumbersome. The alternative for investors is to rely on the legal system.

Default rates remain low but that could change, with credit still tight for the vast majority of borrowers in China. So far, guarantees and other credit enhancements mean that investors in NPL-backed securities haven’t been affected. But these, too, have started falling short. UBS’s Jason Bedford notes that banks have an agency problem because in most cases they appoint themselves as servicers of the bad debt — a fundamental conflict of interest. Since banks are also the biggest sellers of securitized debt, the market can be mispriced to begin with.

Last year, there were a variety of so-called stress events in bad-debt securities: Servicers failed, originators defaulted (resulting in creditors competing for the securitized assets) and interest payments on the notes were missed.

Outside investors landing in such a situation may find there isn’t much left for them to take home. As with valuation, bad-debt recovery in China seems as much folk art as science.

Source: Bloomberg

Latest comments