With China’s economy slowing, banks under pressure to help invigorate growth are rushing to make room on their balance sheets for new lending. That’s unleashed a boom in a corner of the nation’s credit markets.

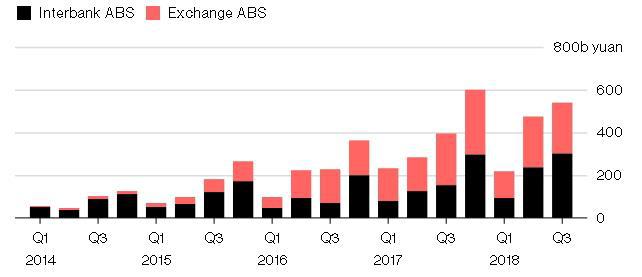

Structured debt sales in China’s interbank bond market jumped in the last quarter to a record 300 billion yuan ($44 billion). Residential mortgage backed securities accounted for about 60 percent of issuance this year through September, from 6 percent in 2015, China International Capital Corp. said and S&P Global Ratings expects this growth to sustain.

The boom in asset-backed securities, which fell out of favor a decade ago for its role in the global financial crisis, couldn’t have come at a better time. China’s central bank has sought to support bank lending to shore up growth as a trade conflict with the U.S. worsens. This month, it will cut the amount of cash lenders must hold as reserves for the fourth time this year.

RMBS Boosts China ABS Sales

China interbank ABS sales hit record in 3Q, with RMBS accounting for about 60%

Source: China Securitization Analytics

“Most Chinese banks are issuing RMBS for the purpose of balance sheet management — selling part of the current loan portfolio through securitization, and reserving capacity for future business opportunity,” said Aaron Lei, senior director at S&P Global Ratings.

Asset-backed securities issued in China’s interbank bond market almost doubled in the June-September period from a year earlier, according to China Securitization Analytics, a platform that aggregates data on ABS products in the country.

U.S. Comparison

Still, the China market is relatively young compared with developed markets such as the U.S. as the former doesn’t have a long track record on deal performance during crises or data on how ABS structures are implemented in a distressed scenario, according to Moody’s Investors Service.

“Because of a longer history, the U.S. ABS market also has a more diverse pool of investors and a deeper and more liquid secondary market,” said Jerome Cheng, senior vice president at Moody’s. “Transaction structures in the U.S. tend to be more robust and have incorporated with different legal and structural protection mechanisms such as the appointment of special servicer.”

With its historical track record, the U.S. market provides investors a “good reference point on not only the volatility of the asset performance but also the implementation of the transaction structure in a distressed situation,” he said.

Mortgage lending is among top assets that banks choose to securitize because RMBS draws good demand from investors for their relatively high credit quality and secondary liquidity, said Yunhui.

China reversed course on securitization in 2012 to allow asset-backed bonds they had banned in 2009 after the products helped spark the global financial crisis. Since then, the market size has hit 2 trillion yuan and China became the second-biggest issuer globally last year, according to Asia Securities Industry & Financial Markets Association.

In the last quarter, Industrial and Commercial Bank of China Ltd. sold 74.7 billion yuan of RMBS while China Construction Bank Corp. and Bank of China Ltd. issued 48.7 billion yuan and 8.3 billion yuan, respectively, according to Zang Yunhui, fixed income director at CIB Economic Research and Consulting Co. in Shanghai.

Source: Bloomberg

Latest comments