China’s smaller banks, among the hardest hit by Chinese government’s crackdown on risky financing, are set for a tougher 2019 as authorities force them to shut business lines that once powered profit growth.

Authorities have ordered the nation’s provincial lenders to limit business to the region they’re based in, or wind down by the end of this year, and have said that some banks expand “blindly.” The new rules will contribute to lower profits at the small banks, which have been already overvalued when compared with bigger rivals, according to analysts.

It could mean another long year for investors in Chinese banks after a bruising 2018 that saw the shares of just five out of more than 40 listed firms register annual gains, according to data compiled by Bloomberg. Faced with a slowing economy, a crackdown on the country’s debt pile and record corporate defaults, the sector is struggling to perform -- a feat made harder by strong government intervention.

“Regulators have spotted hidden risks,” said Sun Lijin, a Beijing-based analyst at Pacific Securities Co. “We’ve been wary of city commercial banks from the very beginning. Many of them have taken on more risk than they understood or could possibly handle.”

The peril stems from off-balance-sheet products that small banks, especially in the rust-belt of the northeast, used to boost lending in other provinces as their home economies slowed. The practice helped assets increase by more than 20 percent each year between 2015 to 2017, twice as fast as bigger rivals, but risk also ballooned.

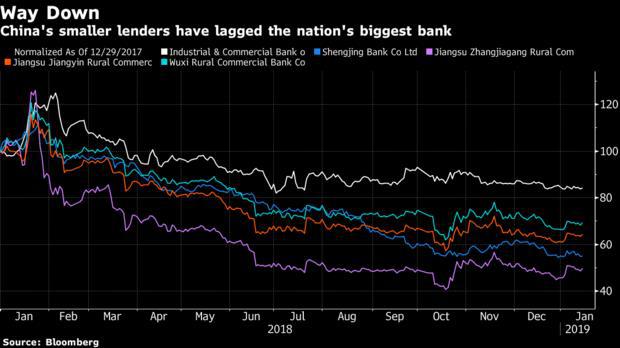

Regional lenders underperformed their larger peers in 2018, with Shengjing Bank Co. down 45 percent in Hong Kong and Jiangsu Zhangjiagang Rural Commercial Bank Co. falling 54 percent in Shenzhen. Even so, analysts said most of China’s small banks are still overvalued. City and rural banks traded at an average 0.8 times their book value, compared with 0.7 times for the four biggest national lenders, which have a more stable profit outlook.

“Unlike bigger banks, city and rural commercial banks are limited in doing business in terms of locations, and therefore at greater risk of credit concentration,” said Liao Chenkai, a Shanghai-based analyst at Capital Securities Corp. “Looking at dividend and growth potential, investing in big banks is also more attractive.”

Publicly-listed city commercial banks will see profit growth slow to 13 percent in 2019 from 15.5 percent last year, according to Essence Securities Co., dragging down the sector’s average to 6 percent from 7 percent.

The central bank’s move to offer cheaper funding to banks that lend to small and micro enterprises will help eligible regional lenders, according to S&P Global. However, investment and loan demand from the private sector will stay low as growth moderates, analysts including Fern Wang wrote in a December report.

Not everyone is so bearish. Analysts at Credit Suisse Group AG said in a Jan. 7 research note that banking sector valuations are at or near their lows, with the industry priced as if bad-debt ratios were higher than they currently are. As such, banks could prove to be a good defensive bet for investors, they wrote.

Among the banks hoping for positive investor interest this year are Jiangsu Kunshan Rural Commercial Bank Co., Bank of Xi’An and Bank of Xiamen Co., who have all applied to go public in China.

But the pressure on bad loans could increase, according to China International Capital Corp., as domestic companies’ profit growth is forecast to slide to nearly zero this year.

“We expect pessimistic forecasts to continue weighing on bank stock prices and valuations,” CICC analysts said in a note. “Investors are deeply worried about the macro economy, but we have not seen policy that can improve pessimistic estimates.”

Source: Bloomberg

Authorities have ordered the nation’s provincial lenders to limit business to the region they’re based in, or wind down by the end of this year, and have said that some banks expand “blindly.” The new rules will contribute to lower profits at the small banks, which have been already overvalued when compared with bigger rivals, according to analysts.

It could mean another long year for investors in Chinese banks after a bruising 2018 that saw the shares of just five out of more than 40 listed firms register annual gains, according to data compiled by Bloomberg. Faced with a slowing economy, a crackdown on the country’s debt pile and record corporate defaults, the sector is struggling to perform -- a feat made harder by strong government intervention.

“Regulators have spotted hidden risks,” said Sun Lijin, a Beijing-based analyst at Pacific Securities Co. “We’ve been wary of city commercial banks from the very beginning. Many of them have taken on more risk than they understood or could possibly handle.”

The peril stems from off-balance-sheet products that small banks, especially in the rust-belt of the northeast, used to boost lending in other provinces as their home economies slowed. The practice helped assets increase by more than 20 percent each year between 2015 to 2017, twice as fast as bigger rivals, but risk also ballooned.

Regional lenders underperformed their larger peers in 2018, with Shengjing Bank Co. down 45 percent in Hong Kong and Jiangsu Zhangjiagang Rural Commercial Bank Co. falling 54 percent in Shenzhen. Even so, analysts said most of China’s small banks are still overvalued. City and rural banks traded at an average 0.8 times their book value, compared with 0.7 times for the four biggest national lenders, which have a more stable profit outlook.

“Unlike bigger banks, city and rural commercial banks are limited in doing business in terms of locations, and therefore at greater risk of credit concentration,” said Liao Chenkai, a Shanghai-based analyst at Capital Securities Corp. “Looking at dividend and growth potential, investing in big banks is also more attractive.”

Publicly-listed city commercial banks will see profit growth slow to 13 percent in 2019 from 15.5 percent last year, according to Essence Securities Co., dragging down the sector’s average to 6 percent from 7 percent.

The central bank’s move to offer cheaper funding to banks that lend to small and micro enterprises will help eligible regional lenders, according to S&P Global. However, investment and loan demand from the private sector will stay low as growth moderates, analysts including Fern Wang wrote in a December report.

Not everyone is so bearish. Analysts at Credit Suisse Group AG said in a Jan. 7 research note that banking sector valuations are at or near their lows, with the industry priced as if bad-debt ratios were higher than they currently are. As such, banks could prove to be a good defensive bet for investors, they wrote.

Among the banks hoping for positive investor interest this year are Jiangsu Kunshan Rural Commercial Bank Co., Bank of Xi’An and Bank of Xiamen Co., who have all applied to go public in China.

But the pressure on bad loans could increase, according to China International Capital Corp., as domestic companies’ profit growth is forecast to slide to nearly zero this year.

“We expect pessimistic forecasts to continue weighing on bank stock prices and valuations,” CICC analysts said in a note. “Investors are deeply worried about the macro economy, but we have not seen policy that can improve pessimistic estimates.”

Source: Bloomberg

Latest comments