As suddenly as it rolled in, the crisis of confidence that shook Chinese stocks last year may be ending.

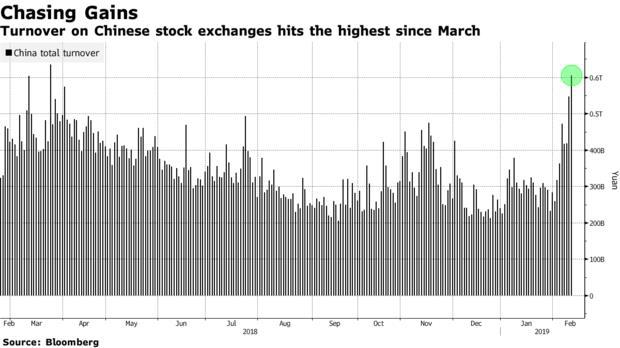

The rally since January has added about $880 billion to the value of the country’s equities, lifting Shenzhen’s risky startups and state-backed giants alike. The rebound has been so quick and widespread that it’s already triggered signs of overheating in four of China’s major benchmarks. The CSI 300 Index’s 14 percent rally is its best start to any year in a decade, and turnover across all exchanges is the highest since March.

While valuations have been low for months, Chinese equities really took off only after another set of weak economic data made monetary policy easing almost a certainty. Gains intensified when the new securities watchdog eased restrictions on trading, encouraging an increase in leveraged bets. Ample liquidity and a streak of foreign buying have fueled volumes.

“It’s essentially a reflection of change in investor expectations,” said Wang Chen, a Shanghai-based partner with XuFunds Investment Management Co. “The rally’s been driven by a return in risk appetite and a valuation catch-up.”

The recovery is an about-face from 2018, when the government’s deleveraging campaign triggered a liquidity crunch and record bond defaults. Sentiment was so bearish after the equity market’s $2.3 trillion rout that average turnover was down to nearly the lowest in four years by December.

Traders are quickly moving on from last month’s deluge of profit warnings and China’s weaker economic growth, focusing instead on all the reasons why the outlook should improve. An interest-rate cut from the People’s Bank of China is on the cards, while next month’s annual gathering of top-level officials may spawn more supportive policies. Even Chinese state media has chimed in, highlighting the growing bull case for stocks.

Next week’s decision by MSCI Inc. on whether to include a broader array of A shares in its indexes may also provide another catalyst.

The concern is that China’s equity rebound is on shaky ground, underpinned mostly by fickle investor sentiment. Evidence of speculative trading has popped up in some of the riskiest parts of the market, and traders are borrowing more cash to chase the rally. Skeptics say only a better-than-expected recovery in profit growth will drive the next leg up.

“The rally lacks fundamental support,” said Jeff Chang, chairman of Cathay Securities Investment Trust Co. in Taipei. “It’s hard to see the indexes move up much higher unless earnings turn out better than expected.”

Depressed valuations keep attracting dip buyers for now. The CSI 300 still trades at less than 11 times projected earnings -- about a quarter lower than last year’s peak. Even the ChiNext Index of small caps is 35 percent cheaper than its five-year average. That means there are still plenty of opportunities in China even if the rebound isn’t as broad going forward, according to Arthur Kwong, head of Asia Pacific equities at BNP Paribas Asset Management in Hong Kong.

“Prices have already rebounded quite a lot and it’s time to be more selective, rather than to buy a whole basket of stocks," he said.

Latest comments